DraftKings is making its own strategic bet on the rise of the US sports betting market

Photo: Curated Lifestyle

19 Nov 2020

Tags

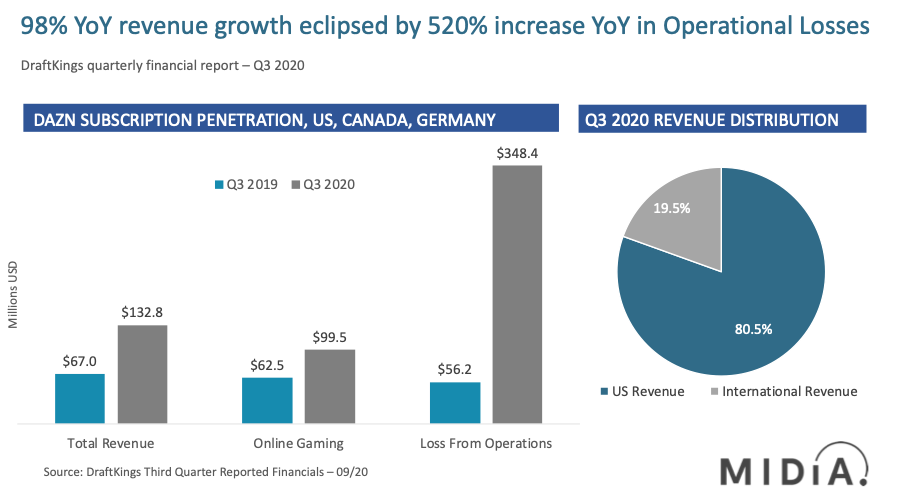

US-based sports betting company DraftKings’ stock value has grown 11% following a strong third-quarter performance in which its revenues increased 98% year on year (YoY) to reach $132.8 million, up from $67 million in Q3 2019.

DraftKings’ success was attributed to the ‘resumption’ of the NBA, MLB and NHL seasons, which had been indefinitely postponed during the pandemic-enforced lockdown. The start of the NFL season also generated ‘tremendous customer engagement’ for the sportsbook in Q3 2020, which witnessed a 64% increase in monthly unique payers on the platform, averaging more than a million unique paying customers each month during the quarter.

DraftKings is the official daily fantasy partner for the NFL, having launched in 2012, and now offers an immersive sports entertainment experience across 15 professional sports in eight countries. In April 2020 DraftKings began trading on the Nasdaq Stock Exchange following a $3.3 billion merger with gaming technology specialists SBTech and investment firm Diamond Eagle Acquisition Corp (DEAC). Leveraging its position as the only US-based vertically integrated pure-play sports betting and online gaming company focused on the American sports fan, the company has updated its projected revenues for the year to $560 million in annual revenues, exceeding earlier forecasts.

Sports betting in the US is still in its infancy, following the 2018 US Supreme Court ruling in favour of allowing US states to decide individually on whether or not to permit sports betting. Legalising gambling opened an untapped and lucrative revenue stream for US companies. Fox Sports’ CEO Eric Shanks has claimed that sports betting / online gaming will be worth $9 billion by 2025, when accounting for wagers, sponsorship and advertising. Jason Robins, DraftKings’ co-founder and chief executive on the earnings call stated that the success following the legalisation demonstrated ‘the effectiveness of our data-driven sales and marketing approach’. This comes atop the sportsbook agreeing several high-profile partnerships including US broadcasters Turner and ESPN (propelling DraftKings’ stock 17%), as well a striking deals with the PGA Tour and MLB-franchise Chicago Cubs.

In September, the company sold an equity stake to retired NBA legend and renowned gambler Michael Jordan, coming onboard as a special adviser, which drove the sportsbook’s shares up 12% following the announcement. The return of live sports coupled with these high-profile partnerships propelled an 87% growth in quarter-on-quarter (QoQ) revenues compared with $70.9 million in Q2 2020 when live sports was frozen.

Featured Report

Defining entertainment superfans Characteristics, categories, and commercial impact

Superfans represent a highly valuable yet consistently underleveraged audience segment for the entertainment industry. What drives this disconnect is the fact that – despite frequent anecdotal use of the term – a standardised, empirical definition remains absent, preventing companies from systematically identifying, nurturing, and monetising th...

Find out more…DraftKings going all in: Revenue growth eclipsed by mounting operational losses

While DraftKings’ revenue growth is strong and accelerating, it is currently running a substantial deficit. In Q3, the sportsbook saw revenue growth of 98%, 75% of which came from its Online Gaming segment, which grew 59% YoY. This is overshadowed by the 520% increase in DraftKings’ loss from its Operations segment, which was $348.4 million in Q3 2020. In its earnings report, DraftKings attributes the cost of revenue increase coming from SBTech following the merger, with $18.8 million in amortisation of acquired intangibles. The sportsbook also attributes $143.3 million to higher advertising spending to increase awareness and engagement, particularly in newly launched US states.

While revenue growth is strong, the use of a special purpose acquisition company (SPAC) vehicle to go public, which allowed DraftKings to begin public trading without holding an initial public offering (IPO), has financial ramifications. Using an SPAC vehicle can be a significant issue for corporate governance, considering later investors become disproportionately penalised by the SPAC sponsor receiving up to 25% of equity at a nominal price, and then potentially cashing in after the IPO. This creates an incentive for the initial investment team to cash in before building a viable sustainable business.

However, DraftKings’ use of an SPAC also reduced the number of hurdles necessary to jump over. The ability to sell new shares while being public significantly increases access to capital via debit issuance for a fast growing organisation with lofty ambitions. DraftKings is arguably now able to invest in its long-term future, roll out into new markets, and increase its spend on advertising, headcounts, marketing technology and support costs. Running a deficit to build long-term sustainability enables DraftKings to make its own strategic bet on the future of the US sports betting market which is still in its infancy given only 5% of US consumers placed wagers on sports in Q3 2020 (source: MIDiA Research). DraftKings is effectively doubling down by positioning itself as a market leader in what is likely to become the largest sports betting market in the world.

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.

The discussion around this post has not yet got started, be the first to add an opinion.