The Three Eras Of Paid Streaming

28 Jul 2017

Tags

Companies

Streaming has driven such a revenue renaissance within the major record labels that the financial markets are now falling over themselves to work out where they can invest in the market, and indeed whether they should. For large financial institutions, there are not many companies that are big enough to be worth investing in. Vivendi is pretty much it. Some have positions in Sony, but as the music division is a smaller part of Sony’s overall business than it is for Vivendi, a position in Sony is only an indirect position in the music business.

The other bet of course is Spotify. With demand exceeding supply these look like good times to be on the sell side of music stocks, though it is worth noting that some hedge funds are also exploring betting against both Vivendi and Spotify. Nonetheless, the likely outcome is that there will be a flurry of activity around big music company stocks, with streaming as the fuel in the engine. With this in mind it is worth contextualizing where streaming is right now and where it fits within the longer term evolution of the market.

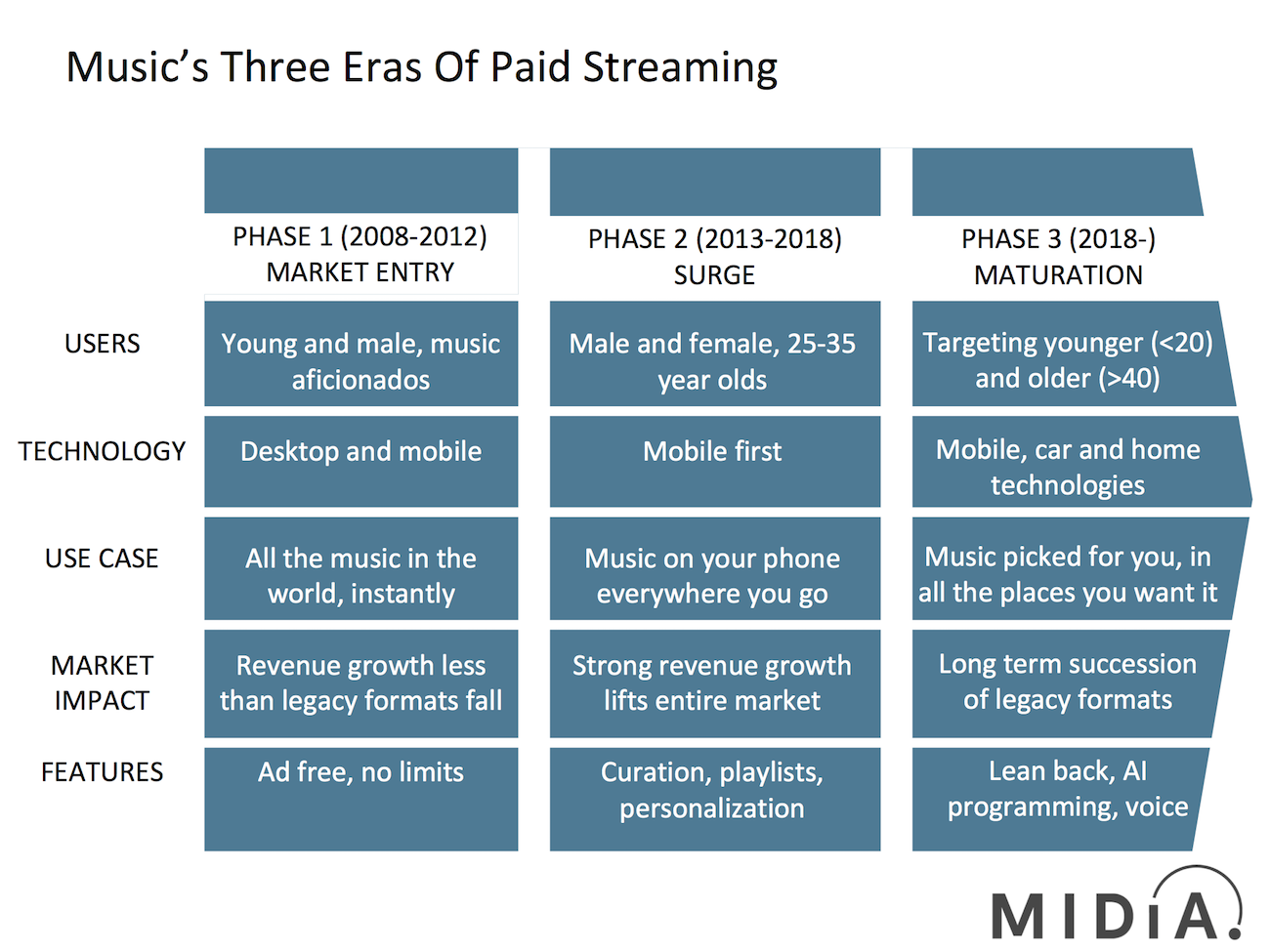

The evolution of paid streaming can be segmented into three key phases:

- Market Entry: This is when streaming was getting going and desktop is still a big part of the streaming experience. Only a small minority of users paid and those that did were tech savvy, music aficionados. As such they skewed young-ish male and very much towards music super fans. These were people who liked to dive deep into music discovery, investing time and effort to search out cool new music, and whose tastes typically skewed towards indie artists. It meant that both indie artists and back catalogue over indexed in the early days of streaming. Because so many of these early adopters had previously been high spending music buyers, streaming revenue growth being smaller than the decline of legacy formats emerged as the dominant trend. $40 a month consumers were becoming $9.99 a month consumers.

- Surge: This is the ongoing and present phase. This is the inflection point on the s-curve, where more numerous early followers adopt. The rapid revenue and subscriber growth will continue for the remainder of 2017 and much of 2018. The demographics are shifting, with gender distribution roughly even, but there is a very strong focus on 25-35 year olds who value paid streaming for the ability to listen to music on their phone whenever and wherever they are. Curation and playlists have become more important in order to help serve the needs of these more mainstream users—still strong music fans— but not quite the train spotter obsessives that drive phase one. A growing number of these users are increasing their monthly spend up to $9.99, helping ensure streaming drives market level growth.

- Maturation: As with all technology trends, the phases overlap. We are already part way into phase three: the maturing of the market. With saturation among the 25-35 year-old music super fans on the horizon in many western markets, the next wave of adoption will be driven by widening out the base either side of the 25-35 year-old heartland. This means converting the fast growing adoption among Gen Z with new products such as unbundled playlists. At the other end of the age equation, it means converting older consumers— audiences for whom listening to music on the go on smartphones is only part (or even none) of their music listening behaviour. Car technologies such as interactive dashboards and home technologies such as Amazon’s echo will be key to unlocking these consumers. Lean back experiences will become even more important than they are now with voice and AI (personalising with context of time, place and personal habits) becoming key.

It has been a great 18 months for streaming and strong growth lies ahead in the near term that will require little more effort than ‘more of the same’. But beyond that, for western markets, new, more nuanced approaches will be required. In some markets such as Sweden, where more than 90% of the paid opportunity has already been tapped, we need this phase three approach right now. Alongside all this, many emerging markets are only just edging towards phase 2. What is crucial for rights holders and streaming services alike is not to slacken on the necessary western market innovation if growth from emerging markets starts delivering major scale. Simplicity of product offering got us to where we are but a more sophisticated approach is needed for the next era of paid streaming.

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.

The discussion around this post has not yet got started, be the first to add an opinion.