Expect Warner Bros. Discovery’s forthcoming full year 2023 results to open up vital strategic choices

Photo: Kent Pilcher

20 Feb 2024

Companies

On Friday, Warner Bros. Discovery (WBD) will announce its full year 2023 financial results to investors in its fourth quarter 2023 earnings call. It is going to make for hard reading by both investors and WBD senior management alike. It is also likely to be the company’s most important set of results since the April 2022 merger between Warner Media and Discovery that spawned the media major. Since that time, the new entity has had to combine managing the assumed Warner Media debt with investing in content and tech to compete in the domestic and international video streaming wars. WBD’s $24 billion market cap (down 60% since April 2022) contrasts with its current $42.4 billion in net debt (debt minus cash on hand). The majority of this is due in more than seven years time, theoretically giving WBD time to course correct – a task made much more difficult by the operating loss of $2.1 billion in FY 2022.

Streaming is now less about content, and more about retention and advertising

From an investors’ perspective, the elephant in the strategic-decision-making room is the direct-to-consumer (DTC) segment that remains loss-leading and commits WBD to a continued aggressive content investment. In 2021, the now WBD CEO, David Zaslav stated that the two combined companies would spend a combined $20 billion annually on content (significantly ahead of Netflix’s $17 billion content spend for that year). The new company would aim to expand its streaming services, to reach a total 400 million global subscribers. By Q3 2023, however, total DTC subscribers were down to 95.1 million (from 96.1 million in Q4 22) and DTC revenues stood at $2.438 billion (slightly down from $2.451 billion in Q4 22).

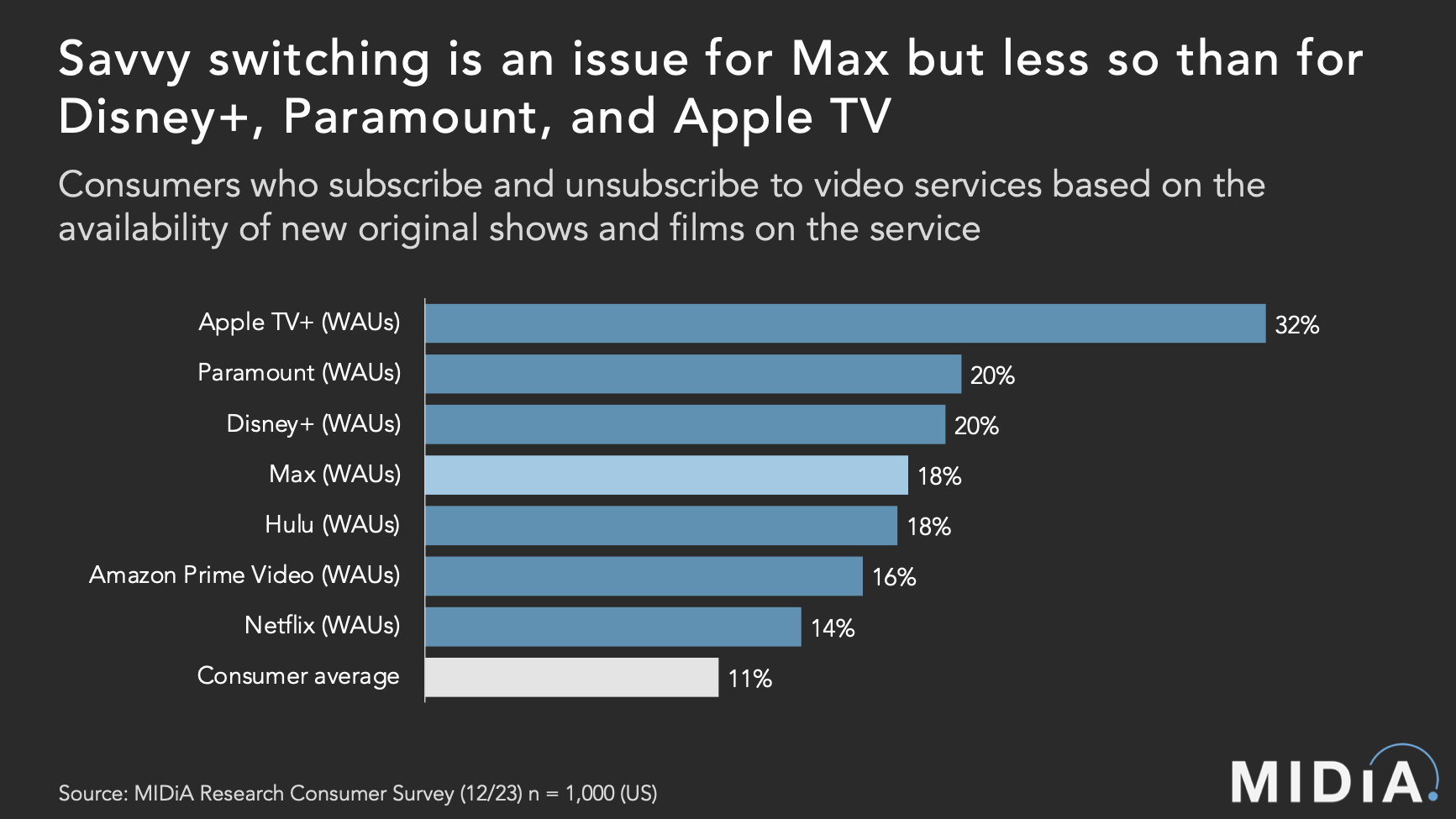

US data from MIDiA’s Q3 23 quarterly consumer survey helps shows why WBD’s DTC business is struggling to grow. 18% of US Max weekly active users (WAUs) engaged in savvy switching (strategically subscribing and unsubscribing based on content availability). While this is above the consumer average of 11% savvy switching, it is comparable with Hulu and only slightly greater than Amazon Prime and Netflix. The good news for WBD is that its savvy switching problem is less severe than for Disney (Disney+ savvy switching stood at 18% for this quarter) and noticeably less than for Apple (Apple TV+ savvy switching stood at 32% for Q3 23).

Featured Report

India market focus A fandom and AI-forward online population

Online Indian consumers are expected to be early movers. They are high entertainment consumers, AI enthusiasts, and high spenders – especially on fandom. This report explores a population that is an early adopter, format-agnostic, mobile-first audience, with huge growth potential.

Find out more…The sliver lining in WBD’s results will likely be the continued strong performance of its ad-supported DTC revenue (which was up 29% in Q3 2023). This will highlight the smart move it made to have an ad-supported component as part of its standard subscription video on demand (SVDO) services from launch despite rival Netflix and Amazon only offering ad-free alternatives at the time. The switch by both leading incumbent SVODs competitors into rolling out ad-supported subscription video on demand highlights the underlying tolerance of consumers for paying less for ad-supported subscriptions (a lesson learnt long ago in WBD’s traditional pay-TV origins).

What is next for WBD?

While Friday’s earnings results will help to clarify the underlying business fundamentals for WBD, it will still leave hard choices for investors and the WBD c-suite. Ultimately, it is likely that a return to more traditional forms of long-term contract will become essential for providing greater predictability in content investment and reducing significant churn costs. Alongside this, a greater focus on playing to WBD’s ad heritage strengths will hopefully help to sustain DTC ad revenue growth amid growing ad competition from Netflix and Amazon.

Ultimately, what WBD does next will have major ramifications for the wider business of film and TV production and monetisation, and ultimately the continued evolution of the streaming TV era. If WBD cannot make the economics of streaming add up then it will need to commit to a radical re-imagining of its intellectual property (IP) for which it remains a leading custodian across entertainment. However this will not be without significant risk as the emerging models of monetising video fandom in the streaming TV era seek to establish themselves.

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.

The discussion around this post has not yet got started, be the first to add an opinion.