Music subscriber market shares 2022

7 Dec 2022

MIDiA has just released its annual ‘Music subscriber market shares’ report and dataset, with data for 23 DSPs across 33 different markets (clients can access it here). Here are some of the key global trends:

Music subscriptions may be recession-resilient, as China leads the way

As the world edges towards a recession, the music streaming market continues to stand strong. Despite indications of slowdown in some markets, the global music subscriber market remains buoyant. Growth, though, is uneven, with a number of leading streaming services outpacing the rest, especially the Chinese ones, which are now setting the global pace.

Home entertainment tends to perform well during recessions, not least because people are inclined to cut down on leisure spend (eating out, bars, clubs, etc.), and thus spend more time at home. In previous recessions, lipstick sales boomed, reflecting their role as an affordable luxury that consumers turn to when they can no longer afford the more expensive luxuries. Music subscriptions have a good chance of playing a similar role in the coming recession.

The early signs are positive (subscriber growth was stronger in the full year of 2021 than 2020), and though the first half (H1) of 2022 growth was down from H1 2021, this reflects the mature state of the streaming market in many markets, as much as it does global economic headwinds.

Featured Report

Splice x MIDiA Sounds of 2026 House on the rise

We zoom in on the trends and microtrends driven by the music industry’s biggest fans and most influential tastemakers: creators. Turn page after page of trends unfolding in real-time and see how Splice’s dataset is the barometer for the state of music today.

Find out more…The evolution of the global music subscriber market is beginning to fork between the leading Western digital service providers (DSPs) and those in Asia – China especially so. Nearly all the leading DSPs continue to experience strong subscriber growth, but none more so than Chinese DSPs Tencent Music Entertainment (TME) and NetEase Cloud Music.

These were the key trends in 2021 and the first half of 2022:

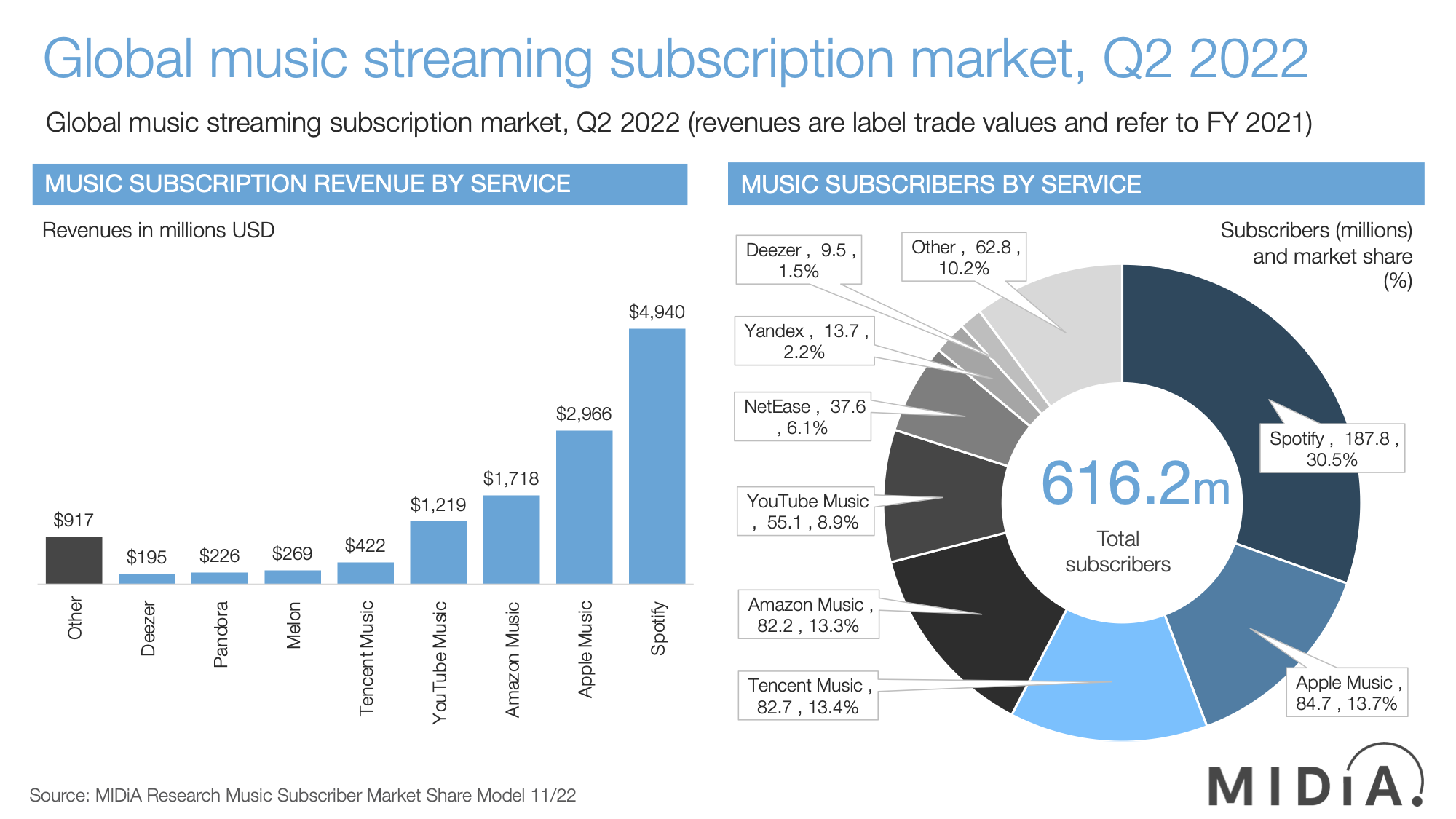

- Subscribers: There were 616.2 million subscribers by the mid-point of 2022, up by 7.1% from the end of 2021. Total net subscriber additions for the first six months of 2022 (42.1 million) were down on the 53.8 million that were added one year earlier, hinting at the slowing global economy. However, more subscribers were added in 2021 than 2020

- Revenue: The $12.9 billion of subscription label trade revenue generated in 2021 was up by 23.1% on 2020, and it was the first year since 2017 that revenue growth exceeded subscriber growth, resulting in a 1.0% increase in global annual ARPU, reaching $22.42

- Spotify: With 187.8 million subscribers in Q2 2022, Spotify remained by far the largest DSP. However, its market share has steadily eroded since Q4 2020, and its Q2 2022 share of 30.5% was down from a high of 33.2% in Q2 2018

- Tencent Music Entertainment and NetEase Cloud Music: Spotify’s declining market share has much to do with the growth of the Chinese market (where Spotify does not operate). In Q4 2021, TME overtook Amazon Music to become the third largest DSP globally, and in Q2 2022 it had 82.7 million subscribers (13.4% market share). China has long been the world’s second largest subscriber market and is on track to soon surpass the US as the world’s largest

- Apple, Amazon, and YouTube: Amazon Music was the fourth largest DSP, with 82.2 million subscribers, and YouTube Music was fifth, with 55.1 million. Both gained share between Q2 2021 and Q2 2022, growing faster than the total market. While YouTube and Amazon both gained share in 2022, albeit it at a declining rate, second-placed Apple Music continued its long-term trend of underperforming the market, with its 84.7 million subscribers recording a 13.8% market share, down 1.2% from Q2 2021.

The global music subscriber market is approaching a pivot point, with the slowdown in mature, Western markets contrasting with more dynamic growth in other regions. It is realistic to assume that the global recession and the organic maturation of the global subscriber market will result in some slowdown of growth in 2023, even if the sector remains otherwise resilient.

The slowing growth should be the catalyst for what needs to come next, especially in developed markets: unlocking growth pockets through differentiation. Western DSPs have managed to grow with largely undifferentiated product propositions. Music rightsholders should explore creative ways in which they can empower their DSP partners with differentiated content assets, enabling them to super-serve specific consumer segments and thus unlock extra growth within them.

If you are not yet a MIDiA client and would like to find out how to get access to this report and data then email stephen@midiaresearch.com

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.

There is a comment on this post, add your opinion.