Netflix Q2 2020 earnings: Lockdown revenue windfall but performance expected to fall

Photo: Netflix

17 Jul 2020

Companies

H1 2020 has been particularly good for Netflix. Q1 2020 saw record subscriber growth of 27.8 million net additions and its original content has dominated viewer interest over the previous six months. The current top three most-viewed Wikipedia TV show pages are all Netflix originals, with D2C challenger Peacock’s Brave New World coming in at fourth place (Source MIDiA Index).

Over this period Netflix has nearly tripled its operating margin from 8.4% in Q4 2019 to 22.1% in Q2 2020. As a result, net income has lept from $587 million in Q4 2019 to $1.4 billion in Q2 2020. However, the financial market’s reaction to yesterday’s Q2 earnings results show that Wall Street is starting to turn negative on the streaming hegemon, with its stock price slumping in after-hours trading yesterday. Netflix’s market guidance for reduced growth in H2 2020 has worried investors, with the company’s stock price down 8% for the week – a $25 billion decline in its overall market capitalisation value.

The abnormal conditions of H1 2020, which were dominated by the most serious global pandemic in a century, led to a 15% increase in entertainment time for house-bound consumers. Streaming services alongside games successfully tapped into this increased engagement. The mainstreaming of subscription video on demand (SVOD) in major markets in Q4 2019 (source MIDIA Research, Brand Tracker) laid the ground work for this subsequent lockdown engagement boost. Older US pay-TV audiences, which have dominated much of western TV strategy for the previous three decades, have now started to become actively courted by the communications majors who are deploying their own D2C video services to counteract cord-cutting and consumer engagement declines. HBO Max and Peacock are being pushed to pay-TV demographics in a way that normalises streaming for the mainstream consumer. Lockdown turbo-charged this and Netflix’s market dominance enhanced its leading position.

Featured Report

India market focus A fandom and AI-forward online population

Online Indian consumers are expected to be early movers. They are high entertainment consumers, AI enthusiasts, and high spenders – especially on fandom. This report explores a population that is an early adopter, format-agnostic, mobile-first audience, with huge growth potential.

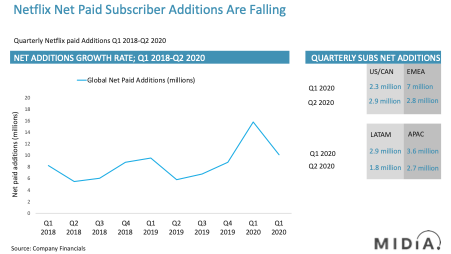

Find out more…However, as a publicly listed, ad-free, paid subscription service, Netflix is judged primarily on its net growth in paid subscribers. The abnormal market conditions of H1 has created what could turn out to be the high water mark for net additions for the streaming service. The increases that would otherwise have come from sustained organic market growth moved forward to compensate for the decline in alternative non-digital entertainment options. The ominous signs of a sustained recession gripping the global economy will further constrain the ability of consumers to add their monthly expenditures by paying for Netflix subscriptions.

With only the US and Canada experiencing a quarter-on-quarter growth in net additions, while the other three regions experienced reduced growth, the H1 front-loading of net additions is now a reality. More worryingly for Netflix, average revenue per user (ARPU) actually declined in its Latin American markets by 8% in Q2 20, underlying the increasing recessionary risks ahead for its subscription revenue growth.

Increased debt interest payments (up 6% in H1 2020) and long-term debt was up by 4% in H1 2020 to $15.3 billion. While Netflix’s overall net margin increase currently offsets this, its fixed costs are rising while its subscriber revenue growth is slowing, flagging increasing margin pressures going forwards. Throw in the increased risks posed by advertising video on demand (AVOD)/ SVOD hybrid challengers such as Peacock, and no wonder that Wall street is increasingly nervous about Netflix’s H2 2020 performance outlook.

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.

The discussion around this post has not yet got started, be the first to add an opinion.