Post-Pandemic Programming

COVID-19 caused dislocation and disruption to the global entertainment business. Now, the recession and the prospect of further pandemic peaks create an unprecedented outlook for entertainment companies. Many of the shifts that occurred during lockdown will define the new market dynamics. The old rule books are being rewritten and new approaches to entertainment business models and experiences will be crucial to move from the holding pattern of survive to the growth mode of thrive. Approaches that worked for decades will no longer work while new innovations will gain traction in a mid-term market that will necessitate an entirely new approach for players across the entertainment industries. MIDiA has kicked off a new programme of research, analysis and insight around these dynamics. We call it Post-Pandemic Programming.

COVID-19 created a mini-recession via lockdown measures, stifling many businesses in an instant, paving the way for the onset of a more traditional, wider recession. All recessions though have uneven impact, affect many companies adversely but some positively. The early signs are that while there were many lockdown losers there were also plenty of companies that fared well, even thrived during lockdown. What was definitely going on, was a reallocation of spend. For example, in Q2 2020 Live Nation and Disney lost $9.9 billion between them compared to Q2 2019. Meanwhile Home Depot increased its revenue by $7.2 billion over the same period. While the comparisons are not perfect, they do illustrate the underlying dynamic well. What is crucial to understanding the post-pandemic period is identifying which of these shifts persist and which revert.

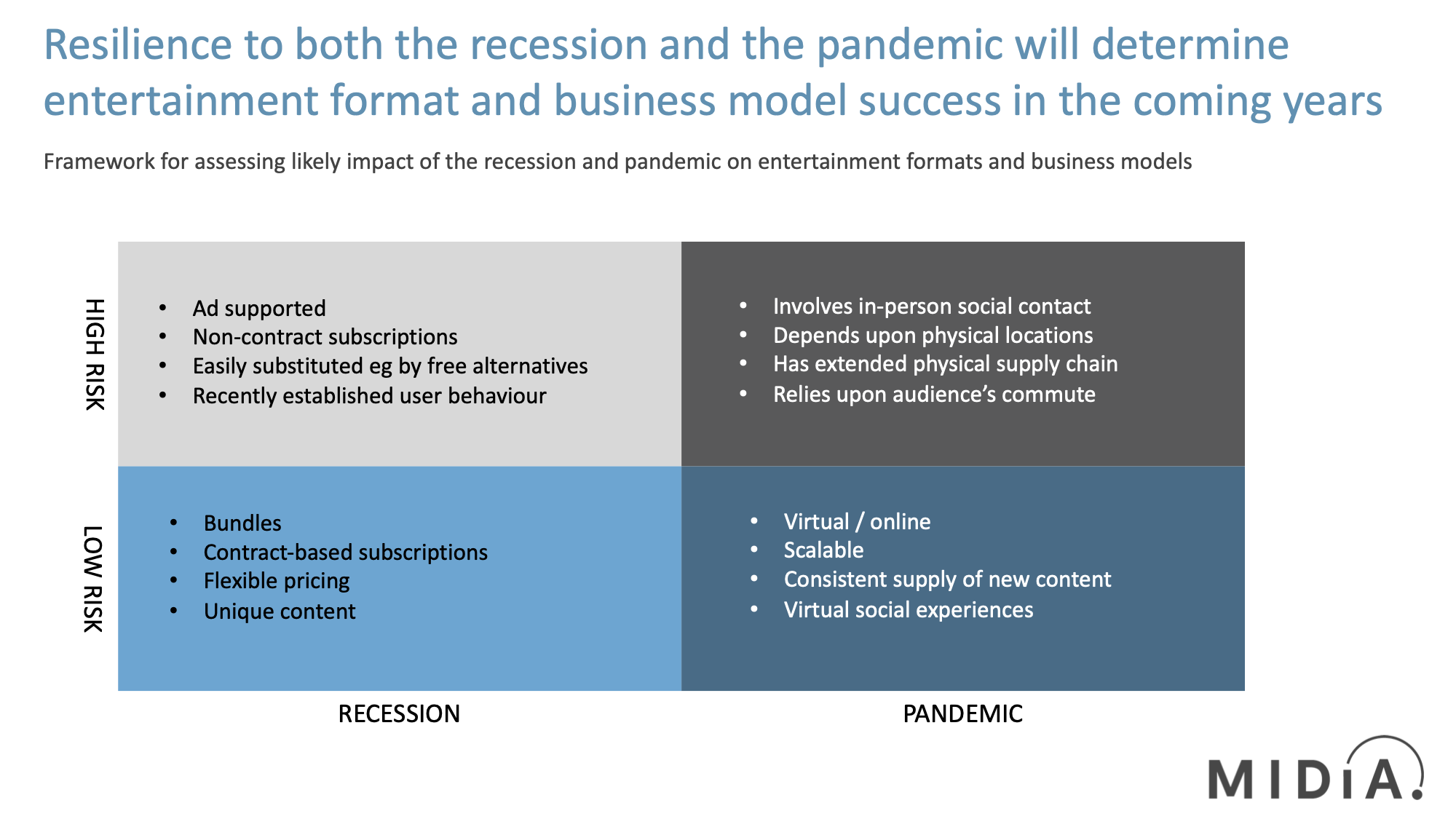

Before that though, the combined impact of the second wave and the coming recession needs to be mapped. To do this, we created a risk framework, looking at what characteristics make entertainment businesses low or high risk, both during a recession and during a pandemic. To understand the coming months, these then need to be overlayed. Companies that have both low recession risk and low pandemic risk will prosper while the adverse is also the case. So, if a company is virtual / online, is scalable, has unique content and is part of a bundle, then it is set to fare well. Enter stage left, Amazon Prime.

Standalone digital subscriptions (e.g. Netflix, Spotify, Xbox Live) are low risk from a pandemic perspective (as the last nine months have illustrated) but the fact they are non-contract based means that they are more vulnerable to churn than say a pay-TV subscription which is contract based and therefore a subscriber has to buy their way out of a commitment (which has the exact opposite of the desired effect of cancelling to save money).

Featured Report

MIDiA Research 2026 predictions Change is the constant

Welcome to the 11th edition of MIDiA’s annual predictions report. The world has changed a lot since our inaugural 2016 edition. The core predictions in that report (video will eat the world, messaging apps will accelerate) are now foundational layers of today’s digital economy.

Find out more…If you are interested in learning more about this research and understanding how music, video, games, sports and media companies will be affected in the coming months, there are two things you can do:

1. Check out our subscriber report

2. Sign up to our free-to-attend webinar on the 10th November

You may need to hurry for the webinar, we are already nearing capacity since promoting it to our clients and newsletter subscribers, but there are still some spaces left.

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.

The discussion around this post has not yet got started, be the first to add an opinion.